You might have missed it all in the chaos of the last week, but the Financial Times published the latest in its series of articles in which a notable figure chats over lunch. The guest diner this time was the former governor of the Bank of England, Mark Carney.

When asked about Brexit, Carney managed to sound diplomatic while also lobbing a hand grenade. “Put it this way,” he said. “In 2016 the British economy was 90% the size of Germany’s. Now it is less than 70%.”

Yet we could be heading for even worse after the Brexit Ultras finally got their hands on the country’s finances and wrecked them in half an hour. The mini-budget was everything they had ever dreamed of. It was the logical conclusion of Brexit, and it tanked the markets, collapsed the pound, almost took down the bond market, sent mortgages and other borrowing costs soaring and guaranteed a British recession.

It was obvious from the very start that Brexit was going to be a disaster for the British economy.

That same Mark Carney had to steady the markets on the day of the referendum result. I was sitting outside the Bank of England in a radio car reporting throughout that day as the pound fell from $1.50 to $1.33 in a matter of hours.

As I said at the time, the international markets do not mark down the value of a currency by 10% because they think the country is going to be 10% richer, they do it because they know it is going to be 10% poorer.

That was just the first reaction to Brexit by a shocked financial system. More shocks have come, and more damage has been done because the Conservative Party has, from the very start, failed to deal with Brexit in an intelligent way. At each step it has made things worse.

It started with the resignation of David Cameron. He could have tried to set the terms of debate based on the narrow victory for Leave and its previous promises. Instead, he allowed the victory to be “owned” by the Ultras, who turned what had been a vote against immigration, and for the NHS, into a total and complete divorce from anything and everything to do with the EU.

Theresa May immediately made things worse by setting out red lines that meant a balanced, mutually advantageous relationship with the EU was impossible. With one negotiating gaffe, May had destroyed not just the bargaining position of the UK but its economy, too. The worse the deal, the bigger the economic damage. It really is that simple.

But the really frightening thing was that the Ultras still wanted May to go further.

The negotiations were mishandled from the start by David Davis, but always at his shoulder he had the Ukippers boasting that the UK would be even better off leaving on WTO terms, that the UK held all the cards, had the EU over a barrel, that the German car makers would come to our rescue.

As a result, the things that were on offer but which the UK spurned were significant; the things it could have asked for and possibly got were huge.

Erasmus, visa-free movement for business purposes, agreement on common regulations, membership of bodies like Reach, agreed veterinary and food standards, cooperation on law and order, data transfers and a dozen more. All of these would have sweetened the pill, saved companies millions of pounds, limited the red tape and ensured good if not brilliant access to our largest and nearest markets.

Yet when this deal was presented to the Tory party, it was not radical enough and May was defenestrated in a coup, led by the very people who had undermined her negotiating position. The victor of the ensuing leadership race was Boris Johnson, who turned out to be a pathetic negotiator who would do and say anything to get a deal done.

In the end, this meant rejecting EU offers to soften the economic blows, placing a border down the Irish Sea, and burning the few remaining bridges between London and the EU.

The economic consequences of Johnson’s “oven-ready” deal were clear enough. The Treasury and various other eminent bodies had done the maths and calculated that this type of deal would cost the UK economy between 4% and 6% of economic growth. Last week, Citi Bank’s top economist claimed that this is probably an underestimate.

This looks increasingly likely; the original calculations seem to have been rather naive in thinking that business would find a way around the new barriers to trade. Instead, they either found a way to do their business in the EU or stopped bothering to trade with it at all.

Nor could the calculations have taken into account either the constant attempts by the Ultras to pick new fights with Brussels, or the UK missing out on hugely important projects such as the Horizon scientific research and innovation programme.

The damage will continue for a long time. Growth for the British economy is now expected to be just 0.8% a year for years to come. This is an economic disaster.

Yet still the Ultras have tried to make things worse, not better. Even before the ink was dry on the treaty, they were at it again. Claiming that international law allowed them to tear up the deal anytime they wanted (which is a complete lie) and that the Northern Ireland protocol meant the UK was still shackled to a corpse.

Who would deal with the UK when it claims to be able to break its word? Who, looking in from the outside, would decide that this is a sensible place to invest? The figures speak for themselves – business investment has flatlined since Brexit, despite ever-more generous tax breaks to encourage it, and the pound has continued to weaken.

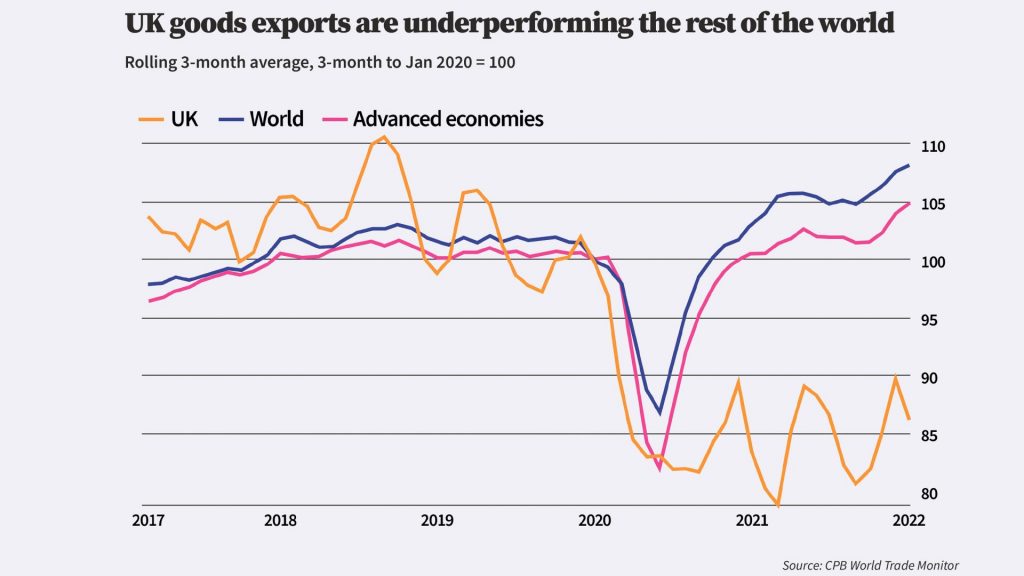

Meanwhile UK trade was and is collapsing; trade with the EU is between 20 and 30% lower than it should be. Our trade deficit is at an all-time high, export data from the continent indicates that huge swathes of the British economy are just not worth dealing with. German exports and imports are soaring – soaring with everyone but the UK that is. The costs and the red tape are too much of a hassle, the game is not worth the candle.

The government response? Blank-faced denial of any problem. So, when Boris Johnson was finally hoist by his own petard, the Conservative Party had a choice for their new leader – a sensible, balanced, realistic Brexit supporter or a convert to the cause, who promised that she would finally give the Ultras all they wanted and more.

I held out a vague hope that Liz Truss was just telling the party faithful what they wanted to hear to win the top job, but the last month shows that she really believed this stuff. Firing civil servants, rejecting and stifling independent and respected advice, betting the house on unfunded tax cuts for millionaires, ignoring the plight of millions. Telling the poor they must work harder for less, slashing benefits; all in an economically illiterate attempt to boost growth.

This was the pure Brexit they had all been waiting for, six long years were predicated on arriving at this moment. The chance to create a Singapore-on-Thames economy, slash all the rules and regulations, cut wages and benefits, reduce the size of government, end the nanny state, trickle-down economics and tax cuts for millionaires. It lasted a week.

For the markets, it was the straw that broke the camel’s back. Six years of failure, lies and fantasies were in the end just too much. One of the few British institutions that still has international credibility, the Bank of England, had to step in just like it did on the first day of Brexit and rescue the government and the country. But even the Bank cannot hold this line much longer.

And yet on the Today programme last Saturday, we first had Sir John Redwood claiming that the key to growth was fracking and more British food production. Dig for Victory is not only the future of Brexit but it will also create a high-growth economy. Right.

Then, when new chancellor Jeremy Hunt was asked about the deep schisms in the Conservative Party, he told Martha Kearney that, to the contrary, “The big divide has been settled inside the Conservative Party and everyone now wants to get on and make a terrific success of Brexit.”

There are none so blind as those who don’t want to see, but in one sense I think we can be optimistic because for the rest of the country the scales seem finally to be falling from their eyes.

Now even some of the commentariat are changing tune: Jeremy Warner dared to tell the Telegraph’s readers that Project Fear had been right all along; Matthew Syed refers to the Tory party being taken over by a “Death Cult”, but elsewhere the IEA, TaxPayers’ Alliance and the shriller supporters of Brexit are doubling down.

They will never give in, they will always say that the “Lost Cause” was stabbed in the back, that Brexit was betrayed or never tried properly, that victory is just one more push away.

But hopefully the mood music is changing, the cleverer commentators are changing sides, as they always do. When they see the bandwagon change direction, they are always the first to jump on.

The cost-of-living crisis, the collapsing services, the economic mismanagement, the six years of broken promises, recession, lost reputation, lost growth, lost power, lost influence; have finally allowed everyone to see the reality.

There is a sunlit upland out there. It is further away than it used to be and harder to reach. But at least we may soon stop marching blindly in the opposite direction.